Sally Blair

&

Associates

Keller Williams Greater Seattle

Main Headquarters

Sally Blair & Associates

1307 N 45th St

Suite 300

Seattle, WA 98103

ph: 360-600-0232

Sally

For Buyers

Articles On This Page:

Prime Time to Buy

Conforming VS Jumbo Loan

The 10 Commandments to Buying a Home

This Month In Real Estate Video

Prime Time to Buy

7 Reasons Why Now Is a Great Time to Buy a Home

Recent history has reframed some of what had long been taken for granted about buying a home. Namely, we’ve learned that even though buying a home remains one of the best and safest investments available, a home should not function as an ATM or a short-term speculation strategy. So, where does that leave us? A lot smarter, able to recognize an opportunity when we see one, and aware of the facts that point to now as the prime time to buy a home.

- Home affordability is at an all-time high. The median mortgage payment on the median-priced home, as a percentage of the median household income, is lower than it’s been in a generation.

- Mortgage rates are at rock bottom. It’s hard to imagine interest rates going much lower, and when they start to inch back upward, monthly payments and total loan costs will spike upward.

- Home prices are back on the rise. After declining for 30 months, home prices are trending back upward. The time to get in the market is now.

- Sellers are motivated. This means that buyers have the upper hand. Sellers are fiercely competing among an excess of housing inventory, which often means buyers have untold choices and negotiating power.

- Financing is readily available. Banks are back in the game and ready to lend to well-qualified buyers.

- Owning vs. renting is increasingly favorable. Since 2009, the average principal and interest payment has fallen below the average rental rates, and the gap is now wider than it’s been in the past 22 years.

- Homeownership is still at the core of the American Dream. Owning a home is critical to financial stability and wealth building. It’s a forced savings account, a place to live, and a fabulous tax deduction.

For more detail, check out Keller Williams Realty’s 7 Reasons Why Now Is a Great Time to Buy a Home! and The Wall Street Journal’s 10 Reasons to Buy a Home.

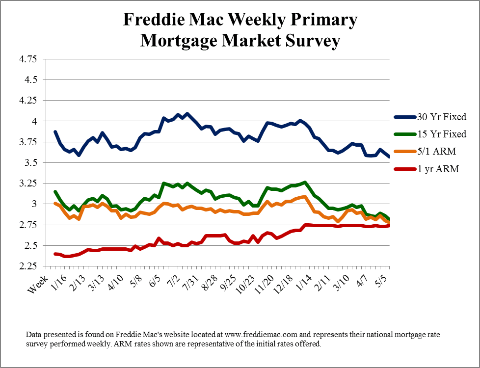

Weekly Mortgage Market in Review | ||||||||||||||||||||||||||||||||||||

The majority of mortgages in the United States are purchased and guaranteed by, Fannie Mae and Freddie Mac. These two government-sponsored enterprises cover almost any mortgage, as long as it follows their “conforming loan” guidelines which include the size of the loan. The maximum amount for a single family conforming loan is $417,000 in most of the U.S.; though in federally designated “high cost” areas, it may be as high as $625,500. When mortgages exceed these thresholds, they receive their “jumbo” status. Recent enhancements to Jumbo lending guidelines have created an outstanding opportunity for your clients to increase their purchasing power, while keeping more of their assets liquid.

As one of the Northwest’s leading mortgage banks, PRM has the products and resources to provide access to these and other equally attractive financing options. If your client is interested in taking advantage of Jumbo loan options or has questions about being eligible for this loan, contact me today! | ||||||||||||||||||||||||||||||||||||

PRM, Your Solution Based Lender | ||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||

Market Comment Mortgage bond prices finished the week slightly lower which pushed rates higher. Rates seesawed back and forth throughout the week within a very narrow range. The Treasury auctions gained more attention early in the week amid no data. The auctions were generally solid except for some mixed demand for the 30 year offering. Stocks were volatile throughout the week. The DOW closed up over 200 points Tuesday only to close down over 200 points Wednesday. Weekly jobless claims were higher than expected at 294K versus 270K. Unfortunately we saw no rate decreases in response. Producer prices rose 0.2% versus the expected 0.3% increase. The core rose 0.1% as expected. Mortgage interest rates finished the week worse by approximately 1/8 to 1/4 of a discount point. Looking Ahead | ||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||

Fed Minutes The Federal Open Market Committee decided in December of 2004 to reduce the lag time between the open market committee meeting and the release of the minutes from six to eight weeks to only three weeks. The minutes from the meeting have the ability to cause mortgage interest rate volatility because they provide more policy details than the standard post meeting release. Most importantly the minutes provide the Fed’s complete economic analysis and the various opinions of individual Fed members. There is typically an overwhelming consensus among the members. However, there can also be dissension, which often causes uneasiness in the financial markets. In the past the release often came and went without much uproar. Lately the financial markets have been so uncertain that every piece of data receives some reaction. Keep in mind that if any of the text seems troubling to analysts you can see market volatility. Remember that mortgage interest rates remain historically favorable. Capitalizing on current rates is a sure thing. | ||||||||||||||||||||||||||||||||||||

Copyright 2016. All Rights Reserved. Mortgage Market Information Services, Inc. www.ratelink.com The information contained herein is believed to be accurate, however no representation or warranties are written or implied. | ||||||||||||||||||||||||||||||||||||

This electronic mail may contain confidential or privileged information and unauthorized use, copying or distribution other than by the intended recipient is prohibited. In the event you received this communication in error, please notify the sender. Unsubscribe Copyright © 2016. Pacific Residential Mortgage, LLC. All right reserved. Credit on approval. Terms subject to change without notice, Not a commitment to lend. Equal Housing Lender. www.nmlsconsumeraccess.org | ||||||||||||||||||||||||||||||||||||

2019

Sally Blair & Associates

1307 N 45th St

Suite 300

Seattle, WA 98103

ph: 360-600-0232

Sally